Account Statement

Account Statement  Capital Gain Statement

Capital Gain Statement  Key Information Memorandum

Key Information Memorandum  PAN Updation

PAN Updation  Register / Modify KYC Online

Register / Modify KYC Online  Nominee Registration

Nominee Registration  Email / Phone Updation

Email / Phone Updation  OTM / eNACH Registration

OTM / eNACH Registration  Voluntary Lock-in for Mutual Fund Folios

Voluntary Lock-in for Mutual Fund Folios  FAQs

FAQs Reach us

Reach us

Cost of Investment Delay

Calculate the difference in portfolio value over time between starting an SIP immediately and at a later date. Understand the consequences of delaying your investment strategy.

-

years

-

Monthly SIP amount can't be less than 10,000

-

years

-

%

-

- vs.

-

years

Related tools

Wealth Planner

Take charge of your financial future with our Wealth Planner. Discover the optimal monthly investments required to achieve your goals with ease.

House Purchase Planner

Planning to buy your dream house in few years? Our Dream House Purchase tool helps you to understand the monthly investment required to achieve this goal.

Vacation Savings Planner

Explore your desired destination with confidence by calculating the recommended monthly savings needed to fund your dream trip. Start investing now and embark on the adventure of a lifetime.

Returns Calculator

Understand the current value, absolute and annualized year-on-year (CAGR) returns on investments made in any of our products via the Lumpsum, SIP, SWP or STP mode.

SIP Top-up calculator

SIP brings consistency. SIP with a top-up feature accelerates your investment commitments to achieve financial goals faster.

Child Education Planner

Secure your child's future by taking control of their higher education expenses. Calculate the ideal monthly investments needed to build a sufficient corpus for their brighter tomorrow.

Cost of investment delay calculator is a financial tool that helps youunderstand the potential financial impact of postponing or not making certain investments on time. It takes into account factors such as the expected rate of return on an investment, the length of time the investment is delayed, and the concept of compounding returns over time. By using this calculator, you can quantify how delaying an investment may affect their ability to achieve your financial goals, such as retirement savings or other investment objectives. It can serve as a useful tool for encouraging timely and informed investment decisions.

The future value of your investment depends on three factors:-

• How much you should invest?

• How much returns you get?

• How long you remain invested?

All three aspects areimportant, if you understand the basic formula for wealth creation:-

Future Value = Invested Amount X (1 + Return)Investment Tenure

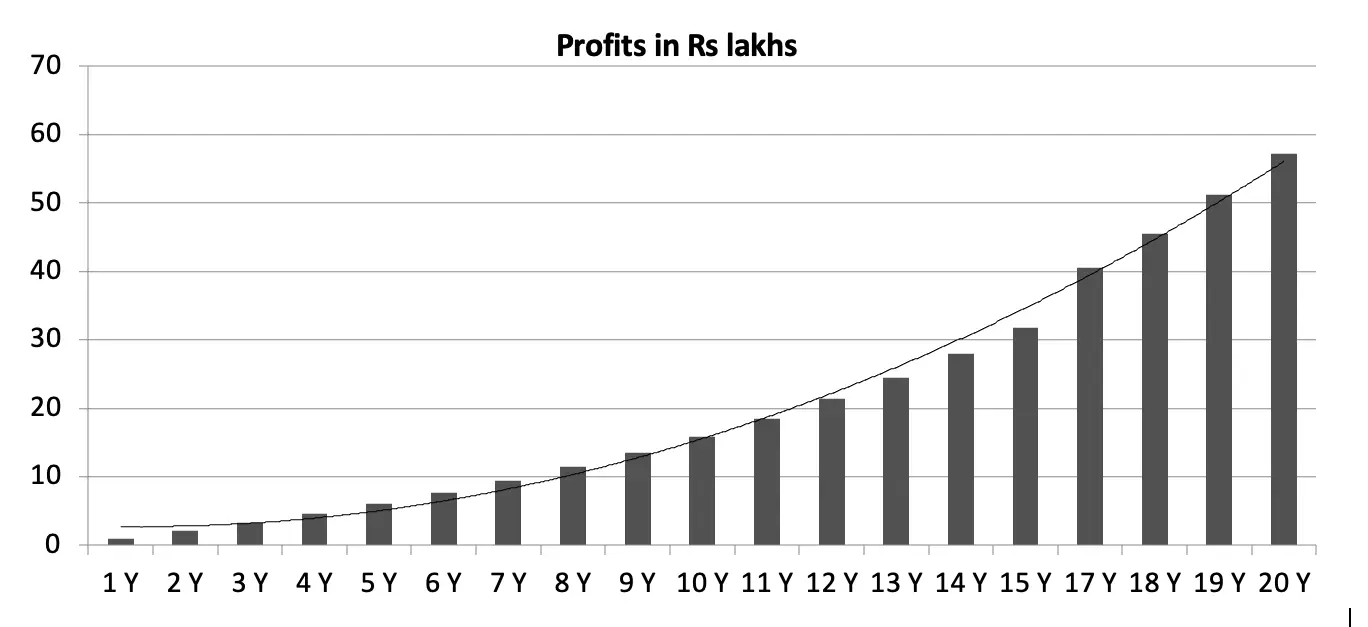

Tenure is the most important factor in the formula of compound interest. Let us assume you invested Rs 10 lakhs and the return is 10% p.a. You can see that profit is not growing linearly. In 3 years profit is around Rs 3 lakhs, but in 20 years profit is around Rs 57 lakhs. This is power of compounding (interest on interest).

If you are investing through monthly SIP, the formula for future value shown above applies for each SIP instalment with a modification for converting years to months as shown below: -

Future Value (for each SIP instalment) = Monthly SIP amount X (1 + Return/12) Investment TenureX12

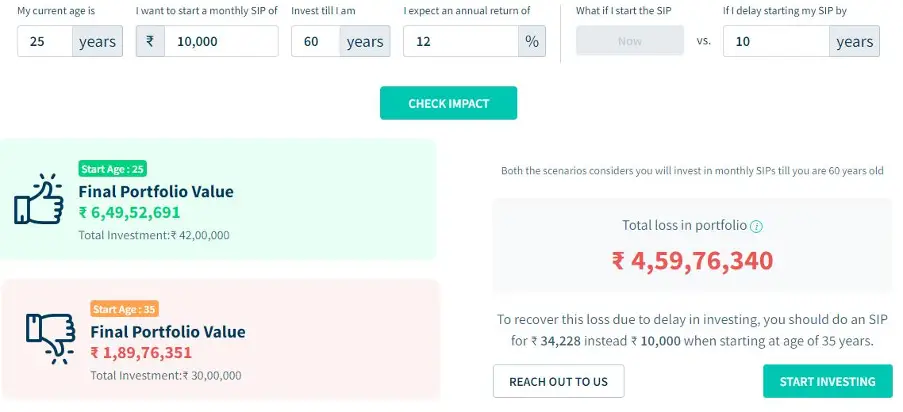

The illustration below depicts how much you can lose in terms of potential wealth creation if you delay your SIP.

You can see that, for the given the assumptions, you are losing nearly Rs 4.6 crores in wealth creation by delaying your SIP by 10 years. In order to catch up, you need to increase your SIP to nearly 3.4 times of what you would have needed if you started early. Cost of investment delay calculator provides valuable insights into the impact of time on investment returns, helping you set realistic financial goals, and make timely decisions. The table below shows how much SIP amount will be needed to reach a wealth creation goal of Rs 1 crore by the age of 50, based on when you start assuming 12% rate of return.

| Age when you start investing | 25 years | 30 years | 35 years | 40 years | 45 years |

| Monthly SIP required to reach goal | 5,322 | 10,109 | 20,017 | 43,471 | 1,22,444 |

Tenure or time makes money work for you through compounding; your financial goals will be easier to achieve if you start early.

1. Financial Awareness: It makes you more aware of the financial consequences of delaying investment decisions, fostering a better understanding of the importance of timely action.

2. Importance of an early start:Making an early start is important in achieving your long term goals. As you progress through life-stages, responsibilities increase and you have to juggle with multiple priorities. An early start will provide you a runway for successful take-off in your investment journey.

3. Avoid wasteful expenditure and save more: Money that is not invested often gets spent in avoidable expenses. If you start saving and investing from a young age, you will get more disciplined in how you handle your finances.

4. Retirement Planning: This calculator emphasizes the significance of early retirement savings and can you plan for a financially secure retirement from a young age. If you delay your retirement planning, you will have to invest much more to achieve your desired retirement goal. It may be challenging at an older age because your will have other priorities like home loan EMIs, children’s higher education etc.

5. Higher wealth creation: You can create substantially greater wealth by starting your investments early. Through mutual fund SIPs you can invest relatively small amounts from your regular savings every month (or any other interval). By investing over long tenures you can benefit from the power of compounding.

The DSP cost of investment calculator (click here) is a tool that helps you understand the potential financial impacts of postponing or not making certain investments. To use the calculator effectively, enter the following details following these steps after opening the calculator:

- Enter your current age here.

- Enter the amount you want to invest on a monthly basis.

- Enter the age until when you want to continue your SIP.

- Enter the expected returns from an asset class. You should enter a reasonable percentage here since an impractical expectation will yield an unrealistic result.

- Enter the number of years by which you want to delay starting your SIP.

Click on ‘check impact’.

You will get to know the cost of delaying the investment versus starting the investment now.

• How much should you enter as SIP amount? You should enter an amount that you will consistently be able to invest every month. If you are new investor estimate your essential expenses (e.g. food, accommodation, utilities, transportation, school fees etc). You should try to save a significant percentage of the balance portion of your monthly income and set aside some part for discretionary spending. Your SIP transaction will fail if you do not have sufficient balance in your savings bank account. Therefore, you need to plan your SIP carefully.

• What should you enter as investment tenure (invest till I am)?Your SIP investments should be tied to your financial goals. Your investment tenure will be the goal timeline. For example, if you are planning to save and invest for retirement, you can put your retirement age e.g. 60 years. If you plan to retire early, input the appropriate age.

• What should you input as expected return? The "expected rate of return" will depend on the type of investments. Different investments have different risk profiles; risk and return are interrelated. You should invest based on your investment tenure and risk appetite. For example, if you are planning your retirement and your current age is 30 years then equity funds can be suitable investment options. If your current age is 50 years or more, you may want to invest in hybrid funds. You should consult with your financial advisor if you need help in making investment decisions. You can refer to long term returns of different asset classes / sub-categories to form your return expectations. It is important to refer to long term asset class returns because short term returns can be misleading.

• What should you input as delay in starting your SIP: You can do sensitivity analysis by varying the input values to see, how different scenarios might impact your results. This can help you make informed investment decisions.

Disclaimer

This tool has been designed for information purposes only. Investor should not consider above as a recommendation for any schemes of DSP Mutual Fund / third party mutual fund schemes. Data captured here is publicly available including information developed in-house. The recipient(s) before acting on any information herein should make his/their own investigation and seek appropriate professional advice. Investors are requested to note that there is no assurance of any returns/capital protection/capital guarantee to the investors in any schemes of DSP Mutual Fund. Past performance may or may not sustain in future and should not be used as a basis for comparison with other investments. The Performance may vary from scheme to scheme and depends upon several factors including load structure, investment framework, AUM, Investment objective, sector diversion, asset allocation & internal risk management parameter. Investor before investing into any kind of mutual fund scheme should read and be aware of scheme specific risk factors including Risk-o-meter of scheme / benchmark, Investment strategy & objective, asset allocation, Load structure, Plan/options available etc. defined in offer documents (Scheme Information Document and Key Information Memorandum) which are available on website. While utmost care has been exercised while preparing this tool, the DSP Asset Managers Private Limited/ DSP mutual Fund nor any person connected does not warrant the completeness or accuracy of the information and disclaims all liabilities, losses and damages arising out of the use of this information.

"All the returns shown are as per the category prescribed in latest AMFI Best practice Guidelines (AMFI BPG) and any such guidelines issued by AMFI from time to time. Category wise calculators used above is to provide conceptual clarity to investors or for educational purposes. Numerical illustrations are being used for SIP / SWP / STP calculators only for the categories to explain the power of compounding. “Past performance may or may not be sustained in future and is not a guarantee of any future returns”. These figures pertain to performance of the categories/situations as prescribed by AMFI by using the compounded annualized growth rate % (CAGR) prescribed against each category/situation and do not in any manner indicate the returns/performance of any of the schemes of the DSP Mutual Fund. Investors are advised to consult their own legal, tax and financial advisors to determine possible tax, legal and other financial implication or consequence of subscribing to any of the units of the schemes of the DSP Mutual Fund. Mutual Fund investments are subject to market risks, read all scheme related documents carefully.

Note: Returns calculated by taking mean of 10-year rolling returns between 01/06/13 and 30/05/23 for various benchmarks. Mean returns are as follows: INR Gold 9.34%; Sensex: 12.64%; Nifty 50: 12.93% and 10-year G-Sec: 7.20%. (This note is as per AMFI BP)"

Get the Insights You Need—Delivered to Your Inbox

Choose the topics that matter most to you.

DSP Mutual Fund is the leading mutual fund investment company in India.

Download Our App

Contact details for complaint resolution: Mr. Santosh Pandey

Investor Relations Officer, DSP Asset Managers Private Limited, The Ruby, 25th Floor, 29, Senapati Bapat Marg, Dadar (West), Mumbai – 400028, Tel.:022-66578000.

.

.

You’ve been unsubscribed

The email address [email protected] has been removed from our mailing list. you will no longer hear from us.