Account Statement

Account Statement  Capital Gain Statement

Capital Gain Statement  Key Information Memorandum

Key Information Memorandum  PAN Updation

PAN Updation  Register / Modify KYC Online

Register / Modify KYC Online  Nominee Registration

Nominee Registration  Email / Phone Updation

Email / Phone Updation  OTM / eNACH Registration

OTM / eNACH Registration  Guidelines for Incapacitated Investors

Guidelines for Incapacitated Investors  FAQs

FAQs Reach us

Reach us

Summary

Learn how to add double engine growth to your portfolio. This blog explains strategies to boost your investments. This blog provides in-depth analysis and practical advice. These funds are suitable for long-term investors looking to save on taxes. They offer a unique combination of tax savings and potential for high returns over time.

Investors put a lot of effort into finding the best performing mutual funds or the next “multi-bagger stock” to get outsized returns than the benchmark. But when there is an instance of massive economic shock, war, or a military coup that destabilizes the entire system, isn’t it natural for most funds and markets to react (fall)? Can this reaction ever be controlled?

One can’t accurately predict the markets or what the future holds for us. But what we can control is our behavior towards the world and our reactions to world events. So, prudent effort from the investor should go towards identifying which investing behaviors or controllable factors can give outsized returns.

While I looked inwards for a possible answer and searched for investing behavior that suits all market climates, I found efficiency in Top-up SIP.

A top-up in SIP is one of the most efficient methods because it creates what I like to call - a double engine growth- in your portfolio in the long run. Why?

- It allows your capital investments to step up automatically

- It allows your returns from the above incremental step-ups to be fueled by the power of compounding

This method is convenient and effective and the best part- it helps form a good habit. In addition to seeking good funds, good returns, and good asset classes, aiming to become good investors by focusing on what one can control with suitable asset allocation towards their goals and risk appetite can go a long way.

Want to understand Top up SIPs better? Watch the video below.

Process for Progress

My belief is that good outcomes are by-products of refined habits. Habits are nothing but automatized behaviors, as the ultimate way to locking good future behaviors is to try to automate them. To put it simply, outcomes are the compound interest of habits. The fruits of forming good habits – eating, sleeping, investing and exercising regularly are never felt on Day 1 and neither does it reveal its power when you compare today’s results with the previous month’s. Being more concerned with your current trajectory than with your current results is a good way to proceed.

Changes that seem small and unyielding at first can compound into miraculous results if you’re willing to stick with the process for years. (Does Time really matter? Read in this blog.)

Changing gears

Having an investment goal brings clarity around the purpose and time horizon within which you want to build your corpus. When you have an objective for which you are building the corpus, SIPs can help you achieve it at a steady pace. Stacking this with a SIP top-up (try our our calculator now) feature might get you to your goals a lot quicker.

The way I see it, the SIP habit must be converted from a normal SIP to a periodic top-up SIP to set yourself up to get to your targets faster.

Ultimately, it is your commitment to the process and longevity that will determine your progress. One of the best ways to build a new habit (SIP top-up) is to identify a current habit (existing SIP) you already have every month and then stack your new behavior on top of it. This is known as habit stacking, which, as behavioral scientists suggest, can be highly effective and easy for converting new behaviors into becoming a habit.

Just like your annual income and lifestyle expenses go up periodically, it is only prudent that your investment allocations rise proportionally through a SIP top-up to meet your long-term goals without any shortfalls.

The purpose of building these habits and tapping into their potential is because motivation alone may not be sufficient to continue playing the long game. The focus shouldn’t be on a single goal alone but the lifestyle of continuous improvement. It will multiply whatever you feed it. One of the hacks is to start with small installments because chances are that you will be able to continue them easily, once initiated.

Shouldn’t I step up my SIP every year after I get my raise?

The reason to start a SIP top-up now instead of doing it after your raise/promotion is that, the human brain is wired to prioritize immediate gratifications over delayed rewards and as you probably know, human beings procrastinate taking action. Humans naturally gravitate toward the option that requires the least amount of work or is the fastest to complete.

One must prime their conditioning to make desired future actions easier and therefore, I say let them be invisible and automated. Doing the right thing should be the easy and default action, and one can always rethink in case you don’t get that raise next year. Therefore, two actions: Start a SIP with a top-up, and work for the raise you’d like, now.

Do it with a financial advisor

Being blessed with a family doctor, skilled auditor, financial advisor, and a dependable network of friends are often overlooked but their value is immeasurable.

The cost of choosing a wrong financial product could end up being much higher than paying a fee to the financial advisor/mutual fund distributor (MFD) for their timely advice and guidance throughout the investing journey.

Investors who haven’t seen many bull and bear markets tend to feel clueless and try to redeem during market shocks, like the COVID-19 fall. Advisors make a difference when they can calm our emotions during those turbulent times and help us plan better instead of us redeeming the entire corpus without any counsel. An accountability partner like a MFD can create an immediate cost to inaction. If you miss your SIP or pause it, the person might call you to know how they can help or find out why the transaction didn’t go through. Share your investment plans with your family. Such things make the costs of violating your promises public and demand an explanation. We care deeply about what our loved ones would think if we broke a promise we made to them. Knowing that someone is watching can be a powerful motivator to not stop your SIP top-up.

Start small, Think Big

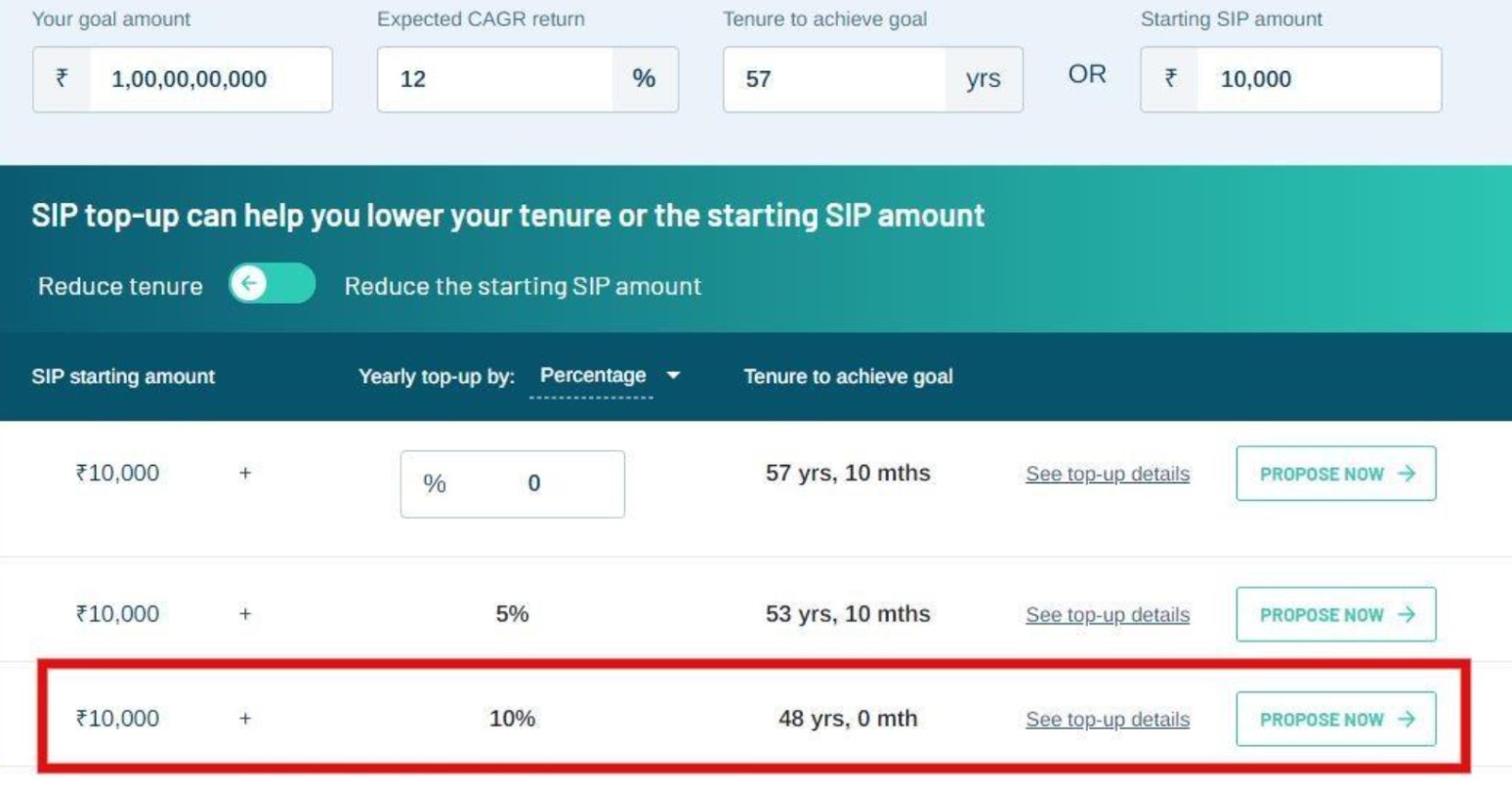

In one of our earlier blogs, “100 crores? It can’t be any simpler for my child”, my colleague Ehsan suggested that if one does a ₹10,000 monthly SIP with a 10% annual top up and manages to earn 12% CAGR, it is possible to build a 100-crore corpus within 48 years.

While the time frame seems too long, I still simply couldn’t believe the 100 crore figure and so HAD TO TRY our new SIP top-up calculator to verify it.

I also checked these figures on my excel sheet to double-confirm the same. Suddenly, it all looked possible. The key thing to note is, that your corpus would be valued at only ~Rs 3.7 crore at end of the 24th year but in double the time horizon, you will reach Rs 100 crore (48th year). The reason why I mention this is that results often take a long time to appear, until one crosses a critical threshold!

The most magical outcomes of any compounding process are ‘delayed’.

Therefore, be patient and restrain yourself from touching the corpus in the early part of your journey so that the compounding process is not disturbed.

Striving for a lifestyle based on good habits like SIP top-ups may seem boring, but it is one of the prudent investing behaviours in the long run.

Industry insights you wouldn't want to miss out on.

Written by

Disclaimer

This note is for information purposes only. In this material DSP Investment Managers Pvt Ltd (the AMC) has used information that is publicly available and is believed to be from reliable sources. While utmost care has been exercised, the author or the AMC does not warrant the completeness or accuracy of the information and disclaims all liabilities, losses and damages arising out of the use of this information. Readers, before acting on any information herein should make their own investigation & seek appropriate professional advice. Any sector(s)/ stock(s)/ issuer(s) mentioned do not constitute any recommendation and the AMC may or may not have any future position in these. All opinions/ figures/ charts/ graphs are as on date of publishing (or as at mentioned date) and are subject to change without notice. Any logos used may be trademarks™ or registered® trademarks of their respective holders, our usage does not imply any affiliation with or endorsement by them.

Past performance may or may not be sustained in the future and should not be used as a basis for comparison with other investments.

Mutual fund investments are subject to market risks, read all scheme related documents carefully.

{kind=link}

Write a comment